Was your roof damaged after a recent storm? Are you wondering what the insurance process looks like when filing a claim for roof damage?

You pay your homeowners insurance to protect your home, hoping you’ll never have to use it. But when you have to use it on a storm-damaged roof, the first and most commonly asked questions revolve around what’s covered, how much you’ll get, and the process.

Unfortunately, not knowing these answers creates confusion, frustration, and the potential to be taken advantage of. You shouldn’t have to deal with this after paying years of insurance premiums.

For over 30 years, the team at Bill Ragan Roofing has taken pride in guiding homeowners through getting their roofs replaced through insurance. That’s why I’ll break down what you need to know about getting a roof replacement through homeowners insurance.

This article answers the following questions:

- Why kind of roof damage does homeowners insurance cover?

- How does the homeowners insurance claim process work for roof damage?

What kind of roof damage does homeowners insurance cover?

Insurance will cover roof damage caused by an extreme weather event or a covered peril. This includes straight-line winds (aka damaging winds) during heavy thunderstorms, hailstorms, snowstorms, or tornadoes.

They’ll also cover damage from fallen trees and limbs that fell on your roof during a storm. As long as there are no exclusions, your insurance will cover a roof replacement if the adjuster finds damage.

How does the homeowners insurance claim process work for roof damage?

The insurance process is long and can drag on if the storm damage in your area is widespread. While you can't do anything about speeding it up, understanding how it works means you're prepared for every step or misstep.

Let's break down the insurance process for roof damage, from identifying storm damage to getting your roof replaced.

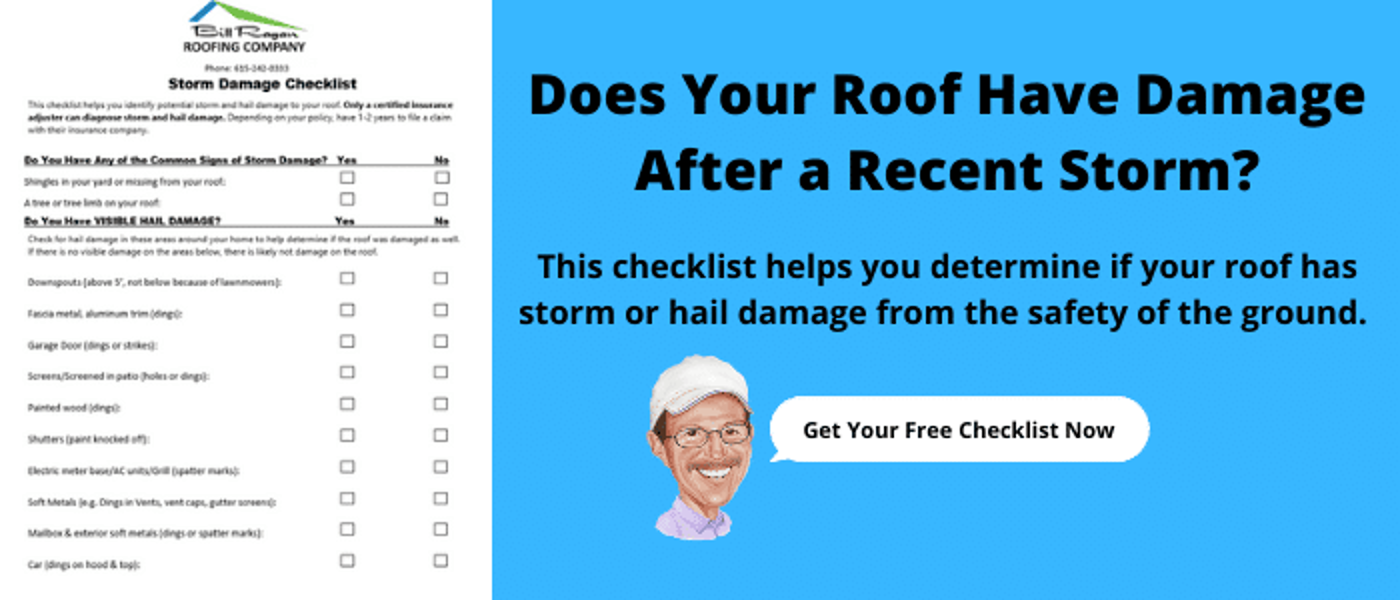

Photo document any potential signs of roof damage

Before doing anything else, you need to determine if it’s worth starting the claim process. Unless you have extensive ladder and roofing experience, you shouldn't get on your roof to check for damage.

Instead, just walk around your property looking for potential signs. For wind damage, look for missing, creased, or sliding shingles while walking around your home.

Identifying hail damage requires being on the roof for a closer look. That's why you should look for collateral damage at the ground level to learn if your roof was possibly impacted.

Below are the following areas to check for collateral hail damage:

- Dents in downspouts (Above 5 feet, so it can’t be blamed on a lawnmower)

- Dings or strikes to your garage door

- Holes in your window screens

- Dings to any painted wood or shutters

- Splatter marks or dings to your electric meter, AC unit, or grill

- Dents to your mailbox and other soft metals on your property

If you’re here, you obviously saw signs of storm damage to your roof. However, it’s also important to photo-document the signs of roof damage as much as you can from the safety of the ground.

Review your insurance policy

After determining if you want to move forward with a claim, you must check your specific policy. Not only will it tell what's covered or excluded, but the type of policy also determines the payout if your roof damage claim is approved.

Actual Cash Value policy

An Actual Cash Value (ACV) policy means the insurance company gives you the depreciated value of your roof at the time of the claim. This policy will never cover the full cost of a roof replacement, meaning you have to cover the rest out of pocket.

Now, some roofers are willing to replace roofs for the amount an ACV policy provides. However, I guarantee they can only do this by using cheap materials and labor.

The low price may seem like a bargain at first, but you’re really just unknowingly setting your roof investment up for premature failure from the start.

Replacement Cost Value policy

A Replacement Cost Value (RCV) policy covers the full or most of the cost to replace your roof with a brand-new version of itself. Once approved, you’ll get a first check for the actual cost value while the insurance company holds back the recoverable depreciation.

After replacing your roof, you’ll get a second check after providing proof that it was done per the claim. Just keep in mind that the insurance company will only pay to restore your new roof to a brand-new version of itself.

This means if you want to add upgrades, like going from 3-tab asphalt shingles to architectural asphalt shingles, you must make up the cost difference out of pocket.

Reach out to your insurance company

After checking your policy, I recommend contacting your insurance company. You’ll pass on all the relevant information, they'll walk you through next steps, and they'll either send out an adjuster or tell you to find a roofing contractor.

Which one they tell you to do is usually based on location, the insurance company, and the number of claims being filed. However, it's also very common for homeowners to get a roof inspection from a roofer first to learn if they actually have damage.

I recommend reaching out to your insurance to ensure you follow their exact process, but I understand wanting to get everything checked out first. Either way, having a trusted roofing contractor handy from the beginning is a good idea.

They’ll be able to guide you and help prove you have a viable claim if there’s actual roof damage. And definitely have your roofing contractor there for the adjuster appointment.

Get a storm damage roof inspection

The next step is getting a storm damage roof inspection to determine if you have a viable claim. The insurance adjuster and roofing contractor will perform their own inspections.

Whoever goes out there first will mark roof areas with missing shingles, granule loss, hail marks, dents in metal, and anything else with chalk. This creates clear reference points when reviewing your claim to determine if the roof has enough damage to warrant a replacement.

After marking the roof damage, they’ll take pictures of everything to submit to the insurance company. They’ll also look for and document any signs of collateral damage on the ground, like you did earlier.

But as I said, it's a good idea for your roofing contractor to be there for the adjuster appointment. Adjusters aren't professional roofers and can miss things because they don’t know where or what to look for.

(Hidden wind damage)

(Hidden wind damage)

It’s also nice to have someone advocating for you on your side. After the inspection, it’s up to the adjuster to approve your claim. Fortunately, you have options if your claim is initially denied.

Receive an estimate for your roof replacement

Once your claim is approved, you’ll get your payout (minus your deductible) for your roof replacement. If you have an ACV policy, you’ll get one check for the value of your roof at the time of your claim.

You’ll then get a quote from your roofing contractor, use the insurance check to cover as much as possible, and then make up the price difference out of pocket. You can also pocket the money instead of putting it towards your roof, but you'll lose coverage because it was already considered a loss.

But if you have an RCV policy, the insurance company provides a scope of work based on Xactimate (or another software) to restore your old roof to a brand new version of itself. The scope of work must be shared with the roofing contractor so they can follow it correctly to ensure you get the recoverable depreciation at the end.

Supplement anything missing from the insurance estimate

The initial price set by the insurance company on an RCV policy is based on general pricing based on the area. Unfortunately, it’s incredibly rare for a reputable roofer to provide a quality roof with the first estimate.

Most insurance estimates don't account for certain line items a roof replacement requires, local codes, and the profit a roofer needs to keep their doors open. That’s why most insurance claims must be supplemented on RCV policies.

A reputable roofing contractor will help you do this, but every company does it differently. I provide a line item checklist so homeowners can go through a claim, add what’s missing, and send it back to their insurance company for approval.

Insurance companies usually provide some pushback, especially around things like overhead. But if you have an RCV policy, supplementing your claim can get most or even the full amount covered.

Get your storm-damaged roof replaced

Once the claim is fully approved, it’s time to pay your deductible and get your roof replaced by the roofing contractor of your choice. If you have an ACV policy, you'll pay your deductible, sign the estimate, use the check provided by insurance to put towards your new roof, and cover the rest yourself.

If this is your situation, this is where the insurance process ends. However, an RCV policy is much different.

After supplementing and everything is agreed on, you'll get the first ACV check from the insurance company to cover your deposit. They’ll look over the insurance paperwork to ensure they follow it correctly before the job, then get to work.

After your roof is replaced, they’ll take photo documentation to prove it was done per the claim and submit it to the insurance company for review.

Pay your deductible and get the recoverable depreciation (RCV policy only)

Your insurance company will review everything to determine if the scope of work was followed correctly. If everything checks out, they'll release the recoverable depreciation check for you to give to the roofing contractor to cover the rest or most of the remaining cost.

If you have already paid the roofer, you'll keep the check. But just know, asking for the recoverable depreciation check without getting the work done is fraud.

So, any payout an RCV policy provides must be used towards your roof replacement. On top of this, it's crucial to remember that you must pay your own deductible, no matter what a roofer may say.

How do you avoid roof damage scams and fraud?

There you have it: the process to replace your storm-damaged roof through homeowners insurance. While the process may seem pretty quick on paper, it’s actually known to drag out and takes patience to ensure you get everything you're owed.

Unfortunately, storms bring out the worst in the roofing industry. Scams and fraud are rampant when it comes to insurance claims for roof damage.

Even worse, they’re never caught until it’s too late, and you’re on the hook. So, before filing a claim or letting a roofer get on your roof, you need to protect yourself.

That’s why I wrote another article with tips to help you avoid the common storm damage insurance scams.

Check out 6 Tips to Avoid Roof Damage Insurance Scams to ensure you don’t fall victim to the bad side of the roofing industry.